Beginning with Early retirement planning strategies, the narrative unfolds in a compelling and distinctive manner, drawing readers into a story that promises to be both engaging and uniquely memorable.

Planning for early retirement is not just about financial readiness; it’s a holistic approach that encompasses lifestyle, psychological well-being, and a strategic investment mindset. Understanding the significance of early retirement can transform your financial future, giving you the freedom to enjoy life on your own terms.

Understanding Early Retirement

Early retirement is a concept that appeals to many individuals seeking to gain control over their lives and finances. It involves stepping away from traditional employment before the conventional retirement age, which is typically viewed as 65. The significance of early retirement in personal finance lies in the ability to allocate resources effectively, enabling individuals to enjoy life on their own terms, free from the constraints of a 9-to-5 job.

The journey toward early retirement is often intertwined with various psychological aspects. Embracing a lifestyle that prioritizes financial independence can lead to a profound sense of freedom and fulfillment. Individuals who retire early can pursue hobbies, travel, volunteer, or spend more quality time with family and friends, enhancing their overall quality of life. However, the transition can also evoke anxiety and uncertainty, as the structure provided by regular employment vanishes.

Thus, understanding the mental shift required for early retirement is crucial for those considering this path.

Financial Independence and Early Retirement

Financial independence serves as the foundation for early retirement, allowing individuals to live off their savings and investments rather than relying on active income from employment. Achieving financial independence typically involves a strategic approach to saving and investing, often characterized by the following principles:

- Living Below Your Means: Maintaining a frugal lifestyle and minimizing expenses is essential. Individuals should focus on essential needs and avoid unnecessary expenditures.

- Building a Robust Savings Plan: Regularly setting aside a portion of income for savings and investments is crucial to ensure a comfortable financial cushion.

- Investing Wisely: Diversifying investments across various assets, such as stocks, bonds, and real estate, can yield better long-term returns and mitigate risks.

- Creating Passive Income Streams: Establishing sources of income that require minimal effort, such as rental properties or dividends from investments, can significantly enhance financial stability.

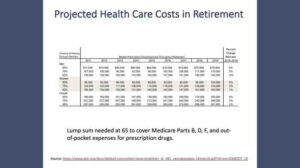

- Planning for Healthcare Costs: Anticipating and budgeting for healthcare expenses in retirement is critical, as these can quickly erode savings if not adequately planned for.

Building financial independence creates a pathway to early retirement, offering a safety net that enables individuals to step away from traditional work life. This journey not only involves financial calculations but also necessitates a shift in mindset, embracing the idea of living with purpose and intention beyond a paycheck.

“Financial independence is not just about having money; it’s about having the freedom to choose how you spend your time.”

Investment Strategies for Early Retirement

Investing wisely is a cornerstone of effective early retirement planning. Utilizing various investment strategies can significantly enhance your wealth accumulation, allowing you to retire earlier than traditional timelines. In this section, we will explore several investment strategies tailored for early retirement, highlighting their potential benefits and associated risks.

Investment Strategies Overview

A diversified investment portfolio is essential for building wealth towards early retirement. The following strategies can help you achieve financial independence:

- Stock Investments: Investing in stocks can provide substantial returns over time, especially when focusing on growth stocks, which are expected to grow at an above-average rate compared to their industry peers. For instance, investing in technology companies like Apple or Amazon has historically yielded impressive returns.

- Mutual Funds: Mutual funds offer a way to pool money with other investors to access a diversified portfolio. They are managed by professionals and can include a mix of stocks, bonds, or other assets, making them a less risky option for retirement savings. Index funds, a type of mutual fund, track a particular index, such as the S&P 500, allowing investors to benefit from overall market growth.

- Futures and Commodities: Investing in futures and commodities can be rewarding but comes with heightened risks. These investments involve agreements to buy or sell an asset at a future date for a predetermined price. While they can lead to substantial profits during market fluctuations, they also carry the risk of significant losses. For example, agricultural commodities often fluctuate based on seasonal conditions, impacting prices dramatically.

- Day Trading: Engaging in day trading involves buying and selling stocks within the same trading day to capitalize on short-term market movements. This strategy can lead to quick profits, but it requires extensive knowledge, experience, and a sound understanding of market trends. Many day traders have reported accumulating wealth at a rapid pace, yet this approach can also result in equally fast losses if not executed carefully.

Benefits and Risks of Futures and Commodities

Investing in futures and commodities can diversify your portfolio and provide opportunities for high returns. However, it’s essential to understand both the benefits and associated risks:

- Benefits:

-

Potential for High Returns:

Prices can increase significantly based on market demand or supply shortages.

- Hedging Opportunities: Futures can be used to hedge against existing investments, protecting your portfolio from price fluctuations.

- Market Accessibility: Futures and commodities markets are accessible to individual investors through various trading platforms.

-

- Risks:

-

Market Volatility:

Prices can be extremely volatile, leading to substantial losses if not monitored closely.

- Leverage Risks: Futures often involve leverage, meaning you can control a large amount of an asset with a relatively small investment, which can amplify both gains and losses.

- Complexity: Understanding the intricacies of futures and commodities requires a steep learning curve.

-

Importance of Mutual Funds in Retirement Strategy

Mutual funds play a critical role in a well-rounded retirement strategy. They provide diversification and professional management, making them an attractive option for many investors. Here are a few key points on their importance:

- Access to Diversification: Mutual funds can invest in a wide range of securities, spreading risk across various asset classes.

- Professional Management: Fund managers make decisions based on thorough research and market analysis, which can benefit those who may not have the time or expertise to manage their investments actively.

- Automatic Reinvestment: Many mutual funds allow for automatic reinvestment of dividends, compounding savings over time.

Insights on Stock Investments

Investing in stocks remains a fundamental strategy for retirement savings due to their potential for growth. Here’s why stocks are crucial in your retirement portfolio:

- Long-term Growth Potential: Historically, the stock market has returned around 7-10% annually when adjusted for inflation, making it a powerful vehicle for wealth accumulation.

- Diversification Opportunities: Investors can diversify their stock holdings across various sectors, minimizing risk while maximizing potential returns.

- Dividend Income: Many stocks pay dividends, providing regular income that can be reinvested or used to cover retirement expenses.

Developing a Comprehensive Retirement Plan

Creating a robust retirement plan is essential for anyone dreaming of early retirement. It requires thoughtful consideration of individual financial goals, spending habits, and investment strategies. This plan should not only focus on accumulating wealth but also on how to manage that wealth during retirement years to ensure long-term sustainability.Developing a comprehensive retirement plan involves several key steps that can help tailor your financial journey toward achieving early retirement.

A personalized approach will factor in your unique situation, including your desired lifestyle, age of retirement, and risk tolerance.

Key Steps to Create a Personalized Retirement Plan

The first step in crafting a personalized retirement plan is to assess your current financial situation. This includes understanding your income, expenses, assets, and liabilities. The following steps can help establish a solid foundation:

- Define retirement goals, including lifestyle expectations and desired retirement age.

- Calculate how much money is needed to support those goals.

- Evaluate existing savings and sources of income.

- Identify potential gaps between current savings and future needs.

A detailed understanding of these components will enable you to chart a path that aligns with your early retirement ambitions.

Organizing a Budget Plan for Early Retirement Goals

Budgeting is crucial for hitting early retirement targets. An effective budget should consider both current expenses and future retirement needs. The objective is to establish a disciplined saving and spending strategy that prioritizes long-term financial health.To do this effectively, consider the following budgeting strategies:

- Track current spending to identify areas for potential savings.

- Set aside a specific percentage of income into retirement accounts each month.

- Plan for unforeseen expenses by building an emergency fund.

- Regularly review and adjust the budget to reflect changes in income or expenses.

This approach ensures that you remain on track toward your early retirement goals while maintaining financial stability.

Comparing Traditional Retirement Planning Methods with Early Retirement Strategies

Traditional retirement planning often focuses on retiring at the age of 65 and accumulating a significant nest egg. However, early retirement requires a different strategy due to the longer duration of retirement and the need for increased savings.Key differences include:

- Higher savings rates: Early retirees typically need to save a larger percentage of their income.

- Investment strategies: Strategies may involve more aggressive investments to grow wealth quickly.

- Withdrawal strategies: Early retirees need to plan for a longer withdrawal period, necessitating distinct approaches to asset liquidation.

Understanding these differences is vital for anyone looking to retire early, as they directly impact how you plan and execute your financial strategy.

Utilizing Tax-Advantaged Accounts in an Early Retirement Plan

Tax-advantaged accounts are essential tools in building a strategy for early retirement. These accounts allow you to grow your savings without immediate tax implications, which can significantly enhance your retirement portfolio.Key types of accounts to consider include:

- Roth IRA: Contributions are made with after-tax dollars, allowing tax-free withdrawals in retirement.

- 401(k): Contributions are tax-deferred, which can be advantageous if you expect to be in a lower tax bracket during retirement.

- Health Savings Account (HSA): This account provides tax-free savings for medical expenses, which can be particularly beneficial in retirement.

Incorporating these accounts into your retirement plan can maximize your savings while minimizing tax burdens, ultimately accelerating your journey toward early retirement.

Final Review

In conclusion, embracing early retirement planning strategies can pave the way for a fulfilling and financially secure future. By understanding the nuances of investment, budgeting, and personal goals, you can confidently take steps towards achieving the dream of retiring early, allowing you to savor life’s moments without the constraints of traditional work schedules.

Common Queries

What is the ideal age to start planning for early retirement?

The ideal age to start planning is as early as your 20s or 30s, allowing ample time to build wealth and adjust strategies.

How much should I save for early retirement?

A common guideline is to save at least 25 times your annual expenses to ensure a comfortable retirement.

Can I rely solely on savings accounts for early retirement?

No, relying solely on savings accounts is not advisable due to low interest rates; diversifying investments is crucial.

What role do health insurance and medical costs play in early retirement planning?

Health insurance and medical costs are significant factors; planning for these expenses is vital to avoid financial strain.

How can I ensure my investment strategies align with my early retirement goals?

Regularly reviewing and adjusting your investment portfolio based on your goals and market conditions can help ensure alignment.