Common retirement planning mistakes can derail even the best intentions for a secure future. Many people underestimate the importance of thorough planning, leading to stress and financial insecurity down the line. As we delve into this topic, you’ll discover the common pitfalls that can impact your retirement savings and overall financial stability.

From failing to diversify investments to neglecting to account for inflation, there are a myriad of issues that can arise if you’re not careful. This overview aims to highlight these mistakes and provide insights on how to navigate the complexities of retirement planning effectively.

Common Retirement Planning Mistakes

Many individuals overlook critical elements when planning for retirement, leading to significant financial pitfalls. Recognizing these common mistakes is essential for ensuring a stable and secure financial future. From underestimating expenses to failing to diversify investments, these errors can profoundly impact one’s quality of life during retirement.One major retirement planning mistake is not starting to save early enough. The time value of money means that even small contributions can grow significantly over time due to compound interest.

By delaying saving, individuals miss out on potential growth, which can result in a substantial shortfall during retirement.

Failure to Create a Comprehensive Retirement Plan

A comprehensive retirement plan includes various components that work together to provide a clear financial roadmap. Without this holistic approach, retirees risk not having enough funds to cover their expenses. The following factors are crucial to consider when creating a retirement plan:

- Estimation of future living expenses: Many underestimate the costs associated with healthcare, housing, and daily living, which can lead to significant financial stress.

- Social Security benefits: A lack of understanding of how Social Security works can result in mismanagement of benefits, leaving retirees with insufficient income.

- Investment strategies: Poor investment choices or overly conservative approaches can yield inadequate returns, jeopardizing the retirement fund’s growth.

- Emergency funds: Not maintaining an emergency fund can lead to financial turmoil when unexpected expenses arise, forcing retirees to dip into retirement savings prematurely.

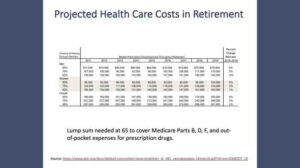

Neglecting Healthcare Costs in Retirement

Many people fail to adequately account for healthcare costs when planning their retirement. With rising medical expenses and the unpredictability of health needs, this oversight can be particularly damaging. Research indicates that healthcare can consume a significant portion of retirement savings.

“The average couple retiring at age 65 can expect to spend approximately $300,000 on healthcare throughout retirement.”

This illustrates the importance of factoring in potential healthcare costs during retirement planning. Individuals should consider supplemental insurance, long-term care insurance, and health savings accounts (HSAs) to cushion these expenses.

Lack of Diversification in Investment Portfolios

Relying solely on one type of investment can leave retirees vulnerable to market fluctuations. Diversification across various asset classes can mitigate risks and enhance the potential for returns. A balanced portfolio that includes stocks, bonds, and other investment vehicles can provide a buffer against economic downturns.The consequences of neglecting diversification can be severe. For example, if retirees invest heavily in a single sector or asset that experiences a downturn, they may face substantial losses, severely impacting their retirement income.

Underestimating the Length of Retirement

Many underestimate how long they will need their retirement savings to last. With increasing life expectancies, it’s common for retirees to spend two or three decades in retirement. This realization necessitates a more extensive savings approach, as funds must last longer than many anticipate. For instance, if an individual retires at age 65 and lives until 90, that’s 25 years of expenses that must be covered.

Planning for such a lengthy duration requires a thorough evaluation of savings, investments, and potential income streams.

Ignoring Inflation’s Impact on Savings

Inflation can erode purchasing power over time, making it crucial for retirees to account for this in their financial planning. Failing to consider inflation can lead to a gradual decline in living standards, as the cost of goods and services increases. Inflation rates have historically averaged around 3% per year. Without factoring this into retirement calculations, individuals risk running out of money sooner than expected, unable to maintain their desired lifestyle.

“Retirement savings should be designed to grow even in retirement, countering the effects of inflation.”

In conclusion, recognizing and addressing common retirement planning mistakes can help individuals create a more secure financial future. By acknowledging these pitfalls and taking proactive steps, retirees can enjoy their golden years with confidence and peace of mind.

Investing Strategies for Retirement

When it comes to preparing for retirement, having a solid investing strategy is crucial. Your approach can significantly impact your financial security in your golden years. While there are numerous strategies available, understanding how they work and how to implement them effectively will help you build a robust retirement portfolio. This section will cover various investing approaches, emphasize the importance of diversification, and explore the roles of mutual funds and stocks in enhancing your retirement wealth.

Types of Investing Approaches

There are several investing strategies that can be particularly beneficial for retirement savings. Each approach caters to different risk tolerances and financial goals. Here are some common strategies:

- Value Investing: This strategy revolves around finding undervalued stocks that are expected to increase in value over time. Investors like Warren Buffet have successfully employed this method, focusing on companies with strong fundamentals.

- Growth Investing: This approach targets companies with significant growth potential. While these stocks may not pay dividends initially, they often provide substantial returns over the long term as the company expands.

- Index Fund Investing: Investing in index funds allows individuals to match the market’s performance by purchasing a broad selection of stocks. This is often considered a lower-risk strategy, especially for those new to investing.

- Income Investing: This strategy focuses on generating passive income through investments in dividend-paying stocks, bonds, or real estate. It’s particularly appealing for retirees seeking consistent cash flow.

Importance of Diversification

Diversification is a key principle in building a retirement portfolio. By spreading investments across various asset classes, you mitigate risk and enhance the potential for returns. The concept is simple: when one investment performs poorly, others can help balance the overall portfolio performance.

“Don’t put all your eggs in one basket.”

A well-diversified portfolio might include a mix of stocks, bonds, mutual funds, and cash equivalents. This balance helps to protect against market volatility and economic downturns. Investors often utilize a diversified approach by considering:

- Asset Classes: Including equities, fixed income, real estate, and commodities to reduce exposure to any single type of investment.

- Geographic Diversity: Investing in both domestic and international markets can shield your portfolio from local economic downturns.

- Sector Diversification: Spreading investments across different sectors of the economy can mitigate risks associated with sector-specific downturns.

Role of Mutual Funds and Stocks

Mutual funds and stocks play vital roles in building retirement wealth for investors. Mutual funds offer a convenient way to invest in a diversified portfolio without having to select individual stocks, making them ideal for those who prefer a hands-off approach. Investors can choose from various mutual funds, including:

- Equity Funds: These funds invest primarily in stocks and have the potential for high returns, making them suitable for long-term growth.

- Bond Funds: Focusing on fixed income, these funds provide stability and regular income, which is beneficial as retirement approaches.

- Balanced Funds: Combining stocks and bonds, these funds aim to provide both growth and income, catering to a wide range of investment goals.

Stocks, on the other hand, are essential for those looking to achieve higher returns over time. Investing in individual stocks allows for greater control and the opportunity to capitalize on market trends. However, selecting the right stocks requires research and analysis.By understanding and applying these investing strategies, individuals can significantly enhance their retirement savings and establish a secure financial future.

Day Trading and Its Implications for Retirement Savings

Day trading, characterized by the rapid buying and selling of stocks within the same trading day, has gained considerable popularity among investors seeking quick profits. However, when it comes to retirement savings, this approach can be a double-edged sword. While day trading may offer the allure of immediate returns, it often comes with significant risks that can jeopardize long-term financial stability.The primary distinction between day trading and long-term investing lies in the approach and time commitment involved.

Long-term investing focuses on building wealth gradually through a diversified portfolio, typically involving stocks, bonds, and other assets held for several years. In contrast, day trading demands constant market monitoring and quick decision-making, often leading to emotional trading driven by market fluctuations. This difference not only influences potential returns but also affects the overall risk profile of a retirement portfolio.

Risks Associated with Day Trading as a Retirement Strategy

Engaging in day trading as part of retirement planning exposes investors to several risks that can undermine financial goals. Understanding these risks is crucial for anyone considering this strategy for their retirement savings.

Volatility Exposure

Day traders often deal with highly volatile stocks, leading to rapid price changes. This volatility can result in significant gains, but equally substantial losses can occur within a matter of hours or minutes.

Emotional Decision-Making

The fast-paced nature of day trading can lead to impulsive decisions based on fear or greed rather than sound investment principles. This emotional trading can severely impact performance.

Transaction Costs

Frequent buying and selling incur substantial transaction fees, which can erode profits. For traders with tight margins, these costs can accumulate quickly and significantly impact overall returns.

Market Timing Risks

Successful day trading relies heavily on accurately timing market movements. Even experienced traders struggle to consistently predict short-term market movements, increasing the risk of losses.

Lack of Diversification

Day traders often concentrate on a limited number of stocks or sectors, exposing their portfolios to higher levels of risk. Long-term investors, conversely, typically diversify across various asset classes to mitigate risk.

“The most dangerous thing you can do is trade with money you can’t afford to lose.”

Impact of Futures and Commodities Trading on Retirement Planning

Futures and commodities trading can also influence retirement planning, presenting unique opportunities and challenges. These trading avenues can offer diversification and potential for high returns, but they carry inherent risks.Investors considering futures and commodities should recognize the following aspects:

Leverage

Futures contracts allow traders to control large amounts of commodities with a relatively small upfront investment. While this can amplify profits, it can also magnify losses, potentially eroding retirement savings.

Market Knowledge

Successful trading in futures and commodities requires a deep understanding of the respective markets, including supply and demand dynamics, geopolitical influences, and economic indicators. Without this knowledge, investors risk significant financial loss.

Volatility and Market Movements

Commodities can experience extreme price swings due to various factors, including weather conditions or global economic shifts. This volatility can pose additional risks for retirement portfolios that are not prepared for sudden market changes.

Regulatory Considerations

The futures market is subject to regulation, and potential changes in regulations can impact trading strategies. Keeping informed about these changes is essential for investors involved in this space.

Long-Term Impact on Portfolio

Incorporating futures and commodities into a retirement strategy may offer unique benefits, such as inflation hedging. However, the balance between risk and potential reward must be carefully evaluated to align with overall retirement goals.

“Diversification is the only free lunch in investing.”

Last Word

In summary, avoiding common retirement planning mistakes is essential for securing your financial future. By recognizing the pitfalls and implementing strategic measures, you can enhance your chances of enjoying a comfortable and stress-free retirement. Remember, the sooner you start planning and investing wisely, the better prepared you’ll be for the years ahead.

Expert Answers

What are some common retirement planning mistakes?

Some common mistakes include not starting to save early, failing to account for healthcare costs, and neglecting to diversify investments.

How can I avoid making these mistakes?

Start planning early, educate yourself on investment options, and consult with a financial advisor to create a tailored plan.

Is it too late to plan for retirement if I’m nearing retirement age?

It’s never too late to start planning; however, the earlier you start, the more options you have to secure a comfortable retirement.

What role does inflation play in retirement planning?

Inflation can erode purchasing power, so it’s crucial to factor it into your retirement savings goals and investment strategies.

Should I consider day trading as part of my retirement strategy?

Day trading is generally risky and not advisable for retirement savings; long-term investing is usually a safer and more effective approach.